")

September 26, 2025

Utility-scale segment drives surge with 4.9 GW added; Texas, California, and Arizona each top 1 GW as residential storage doubles year-over-year

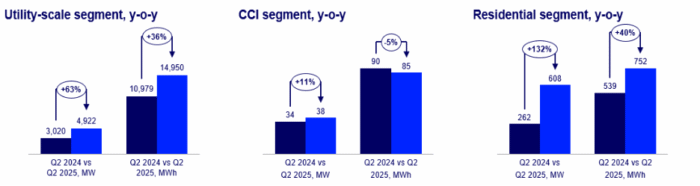

The U.S. energy storage sector posted its strongest quarter on record in Q2 2025, adding 5.6 GW of new capacity, according to the latest U.S. Energy Storage Monitor from the American Clean Power Association (ACP) and Wood Mackenzie. Most of that momentum came from the utility-scale segment, which logged 4.9 GW of installations, enough capacity to cover peak demand for 3.7 million homes.

Utility-scale storage dominates new capacity

Texas, California, and Arizona each added more than 1 GW of large-scale storage last quarter, reflecting the steady role batteries now play in managing grid stress. The Southwest Power Pool (SPP) also showed renewed life, with Oklahoma bringing three projects online—the region’s first since 2022.

In the Southeast, vertically integrated utilities are leaning harder into storage, with Florida and Georgia receiving major forecast upgrades thanks to aggressive procurement activity.

“Energy storage is being quickly deployed to strengthen our grid as demand for power surges and is helping to drive down energy prices for American families and businesses,” said Noah Roberts, ACP’s vice president of energy storage. He added that while regulatory uncertainty lingers, domestic manufacturing of grid batteries is scaling fast enough to meet 100% of U.S. demand in the years ahead.

Residential and CCI markets expand

The residential sector added 608 MW in Q2, more than doubling year-over-year and posting an 8% increase from Q1. Most growth came from California, Arizona, and Illinois, with higher-capacity systems gaining share as attachment rates climbed.

The commercial, community, and industrial (CCI) segment expanded modestly at 38 MW, led by California and New York, though Illinois also showed progress. Policy and cost hurdles continue to slow community storage uptake despite the growing need for neighborhood-scale solutions.

Headwinds on the horizon

Despite near-term growth, the report projects utility-scale storage could dip 10% year-over-year in 2027, largely due to uncertainty over pending Foreign Entity of Concern (FEOC) regulations that will dictate eligible battery cell sourcing for the Investment Tax Credit (ITC).

“All segments of the storage market are feeling both opportunity and risk,” said Allison Feeney, research analyst at Wood Mackenzie. “Residential storage is expected to outpace solar because of stronger policy resilience and consistent ITC access. But pricing pressure, FEOC rules, and sluggish community storage deployment could slow overall growth.”

Allison Weis, Wood Mackenzie’s global head of storage, noted that the One Big Beautiful Bill Act preserved the ITC, but compliance hurdles remain. “A rush to start construction under today’s regulatory certainty is boosting the near-term forecast. Projects that don’t meet milestones by the end of 2025 face real exposure to policy changes.”

Looking ahead

The report forecasts the U.S. market will reach 87.8 GW of cumulative storage by 2029, driven by utility and residential adoption. But headwinds could trim as much as 16.5 GW from the five-year outlook if supply shortages and permitting delays persist.