Earlier this week, the U.S. Energy Information Administration (EIA) released a preview of the changes the U.S. power grid is likely to see over the next year. This data is based on information provided to the Department of Energy by utilities and plant owners who were asked to estimate when planned or under-construction plants will come online. EIA uses that information to estimate the total new capacity that is expected to be activated over the next year.

Obviously not everything goes according to plan. Capacity estimates represent production output if the factory were to run non-stop at full power. Still, the data tends to show what public works are spending their money on, helping to highlight trends in the energy economy.

Big change

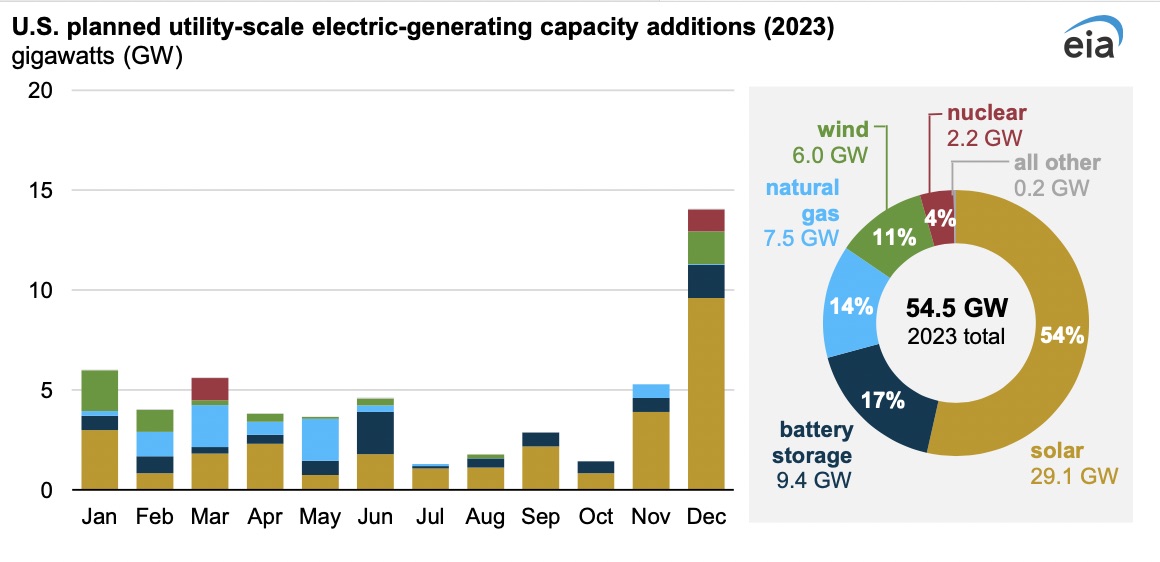

A similar report last year highlighted that solar power will provide nearly half of the 46 gigawatts of new capacity added to the US grid. This year, the grid will add more electricity (just under 55 GW), and solar will more than half that to 54%. In most parts of the country, solar power is currently the cheapest way to generate electricity, and the addition of the grid reflects that. The EIA also shows that at least some of these projects have been delayed due to supply chain disruptions caused by the pandemic.

This year’s new grid addition looks as golden as the sun. Additions are always part of this tax year as he peaks in December.

As a typical example, Texas and California will account for the majority of the 29 GW of new capacity, with Texas alone adding 7.7 GW and California adding another 4.2 GW.

Another trend that is evident is the reversal of the massive expansion of natural gas use following the development of fracking. Last year, natural gas power generation accounted for he 9.6 GW of new capacity. This year, that figure he has shrunk to 7.5 GW. And surprisingly, EIA shows that 6.2 GW of his natural gas generating capacity will be shut down this year. If current trends continue, natural gas capacity could actually decline next year.

The last big trend is the rapid growth of batteries. They don’t produce electricity, but they increasingly offer a function equivalent to a power plant in terms of sending power to the grid when it’s needed. No matter how you look at it, they are booming, up from 11% (5.1 GW) of new capacity last year to 17% this year. At 9.4 GW of new batteries, the addition almost doubled in just one year, putting him in second place in new battery capacity, ahead of natural gas.

and the rest

This doesn’t represent a trend, but there is also big news about nuclear power. His last two reactors, which were under construction at the Bogle Site in Georgia, will be operational. Their operator expects one of the 1.1 GW plants to come online in March and a second in December. Given the plant’s history of delays, it wouldn’t be surprising if the latter slipped into next year.

Even if all goes well, it’s unlikely we’ll see any nuclear additions until the end of the decade. It seems unlikely that it will be completed on time.

Another major source of additional supply, wind power, appears to have entered a period of stagnation. New construction surged at the beginning of the decade before the tax credit expired. However, although this credit has been restored by anti-inflation laws, construction of new facilities has not returned to previous levels. Only 6 GW of new wind power is expected this year, a slight decrease from last year. Things could turn around in the late 2000s, as planners take into account inflation-reducing laws and construction of offshore wind farms begins.

The final part of the story is the continued decline of coal-fired power plants. Nothing new will be completed this year, and nothing is planned. In contrast, about 9 gigawatts of existing coal facilities will be closed. Even if the environmental concerns it creates aren’t fully factored into the cost of coal-fired power, the economy is simply brutal to incumbent operators, who are rapidly exiting the market.